The introduction of a split payment mechanism has been discussed for a long time now. We wrote about it in June last year (20/2017). The new law was meant to be valid from 1 January 2018. Now we know it will be valid from 1 July 2018.

The split payment mechanism assumes every entrepreneur has at least two accounts. The first one is an ordinary bank account, whose rules of operation have not changed in relation to what bank accounts are like today. The other one is, however, a VAT account, which shall be something entirely new. It will still be the entrepreneur's account, but the possibilities of having the means gathered there at one's disposal shall be largely limited. It is worth noting it does not by any means imply that a fiscal organ shall have the VAT account at its disposal. The owner of the account has the right to pay to another entrepreneur for the former's liabilities on account of goods or services used in the amount of VAT, by means gathered on the VAT account, or, alternatively, pay for their liabilities on account of VAT towards the Revenue (including the amount of interest or potential sanctions).

The main rules of the split payment functioning

An optional character

The person purchasing a specific product or service may - but does not have to - pay the seller the VAT amount found on the invoice through the VAT account. Also paying for liabilities towards the Revenue may be done via this account or via an ordinary bank account. The taxpayer has complete choice in this respect. They may as well pay part of the amount from one account, and the other part from the other. Neither the seller, nor the Revenue can interfere with the way the purchaser of goods and services shall pay for their liability. It is well worth noting there are possible arrangements based on a civil law contract, whether and in what way the partners shall use the VAT account in mutual settlements. The fact of not taking advantage of the split payment should not be negatively assessed by fiscal authorities without a more thorough analysis of the specific case.

Settlements in PLN

What is important, a VAT account can be managed only in Polish currency. When it comes to currency accounts, a separate VAT account shall not be opened. The introduction of VAT current accounts would be related to a very high cost on the part of banks (thus in the longer-term perspective, the cost would be placed on the customers).

A lack of additional fees or contracts

The opening of a VAT account shall not require the signing of any additional contracts with the bank. Also, managing the account shall not be related to any additional fees or commission to the benefit of the bank (at least not directly). No payment instruments shall be issued to the VAT account, e.g. payment cards. The interest on the account or the technical aspects related to its management such as information on the balance sheet, shall depend on the contract concerning the main (ordinary) account the entrepreneur has signed with the bank.

One invoice – one transfer

One transfer will not be sufficient to make payments to a few partners, or even to the same partner, but resulting from a few invoices. Mass transfers are out of the question. On the other hand, in a divided payment, only selected invoices of a particular partner shall be made payable, or even only selected items from one invoice.

Among the data to be indicated upon making the transfer, the following information is to be found:

- the partner's Tax Identification Number;

- the gross amount as well as the VAT amount;

- the invoice number the transfer concerns.

The sole making of the transfer shall take place using a dedicated transfer message made available through the bank, technically it will still be only one transfer.

The accelerated as well as "traditional" reimbursement

The taxpayer, upon the submission of a VAT declaration, shall be eligible to apply for the reimbursement of the means resulting from a surplus of the input tax over the tax due within the 25-day-period, if the means are to be reimbursed to the VAT account.

The entrepreneur may also apply to have the cost reimbursed to their usual account, whereby however, the fiscal authority has 60 days to verify the validity of the application as well as its realisation. Within the 60-day period, a refusal of reimbursement is possible, when the taxpayer - on the day of issuing the decision - has VAT tax arrears or if the head of the tax office has a justified belief that the taxpayer will not fulfill their VAT-related commitments, that there probably will be arrears in the future or that there will be sanctions based on the VAT regulations.

The difference as compared to the rules to date shall be that within 60 days there will be a final decision, pronouncing the final judgment (without deceiving the taxpayer by means of several examinations delaying the whole procedure).

Not that much into finance and taxes but overwhelmed by documents you’re not sure how to read?

FIND OUT MORE

Incentives for entrepreneurs

Apart from an accelerated reimbursement of the tax surplus to the split payment users, punitive rates on the tax liability arrears (150%), or sanctions in the form of additional liabilities (20%, 30% or 100%) shall not be applicable. Joint and several liability towards the deliverer of sensitive material shall not be valid. It strictly concerns the liabilities settled from the VAT account.

The legislator attempts to encourage the taxpayers to use the split payment mechanism.

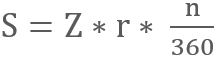

Another incentive is lowering the tax in case of the latter being paid before schedule. The lowered amount will be calculated by means of the following mathematical formula:

where:

S = the amount of decrease

Z = the amount of tax as results from the declaration

r = the NBP reference rate in force two days prior to the date of payment

n = the number of days prior to the date of payment (not counting the day agreed for debiting the accounts)

The real "bonus" shall be low in most cases.

The future of split payment

The Ministry of Finance is preparing a real surprise. Soon, binding explanations on split payment shall come into force. It is a precedent that KAS sees the necessity to explain regulations before they come into force. It would be good if such a mode of change in tax regulations became the norm.

In the future, the mechanism of split payment shall become obligatory at least for some taxpayers. Possibly, from 2019 onwards, the mandatory split payment shall become obligatory for taxpayers trading in sensitive goods, who nowadays fall under the category of joint and several liability (attachment no. 13 of the Act on VAT). For it to happen, the European Commission has to give consent. The talks are ongoing.

Subscribe to RSM Poland Newsletter to stay up-to-date on all legal, financial and tax matters. Benefit from the expertise of our professionals.

Subscribe

If you have any questions or need to discuss the topic, you are strongly encouraged to contact our expert, Przemysław POWIERZA:

e-mail: ekspert@rsmpoland.pl

tel. +48 61 8515 766

fax +48 61 8515 786